This post may contain affiliate links(s). An affiliate link means I may earn advertising/referral fees if you make a purchase through my link,

without any additional cost to you. It helps to keep this site afloat. Thank you in advance for your support. If you like what we do here, maybe buy me a

coffee.

CIPA March 2018 - A new hope for ILC's

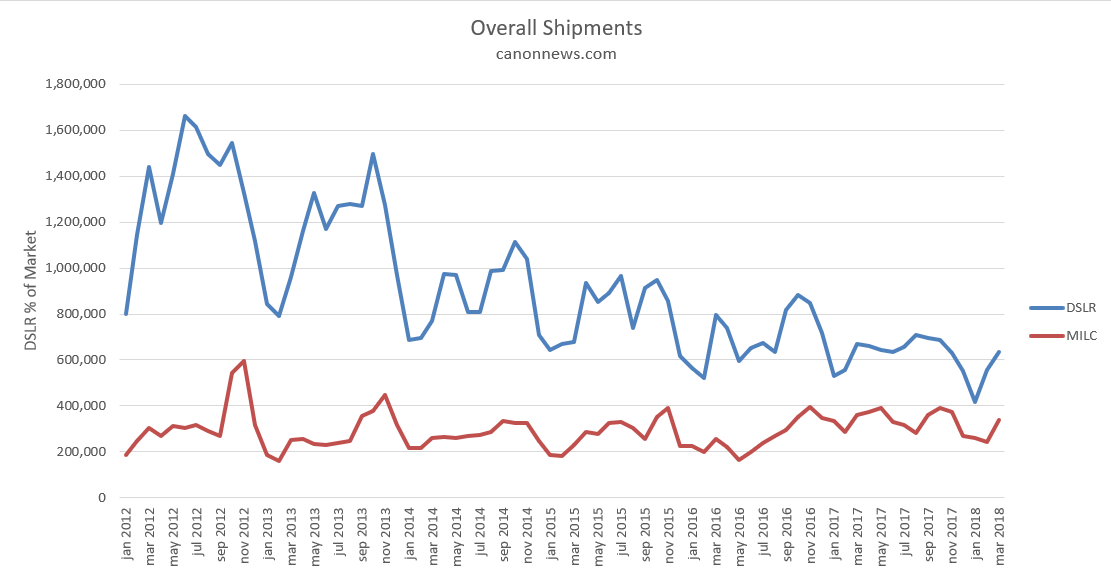

With the third month of the year reported in today, we start to see signs of an overall stabilization in the shipments for ILC’s.

With the Kumamoto earthquake finally in the past, we see that the shipments overall for this month is almost that of the year past and maintain a little consistency from month to month at around 95% of last year’s March shipments. Japan for the first time ever has shipped more Mirrorless than DSLR’s which is an interesting notable that will have to be watched in the coming months ahead.

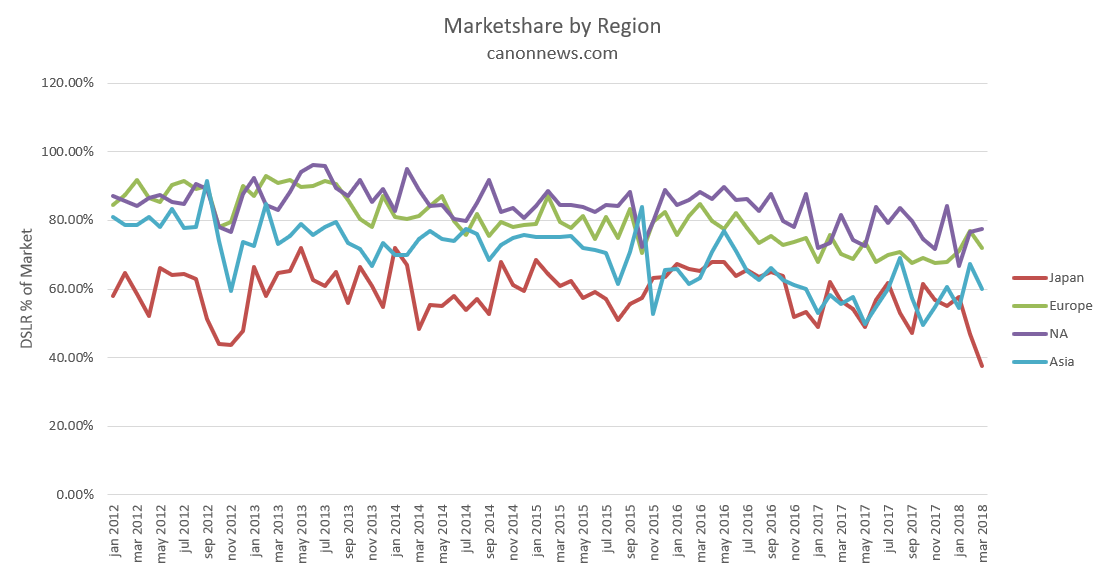

DSLR’s continue to ship less, thereby raising the mirrorless market share. This month instead of looking at percentages, we’re going to look at units, where it shows a far more startling trend for DSLR’s over the last 4 or so years than it does if you looked at percentages of market.

From this graph here, we can see that the clear majority of unit loss on an annual basis has been the loss of shipments of DSLR’s.

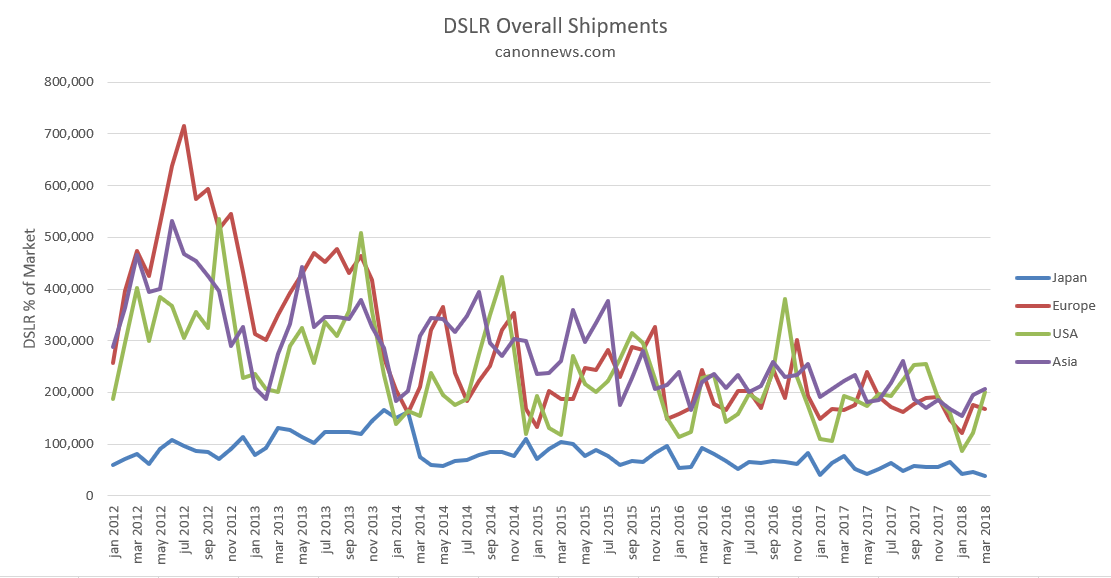

There are several contributing factors to this that you must consider while looking at this chart.

- DSLR product releases because of product maturity are longer.

- Sony got out of the DSLR game around the end of 2014 in a big way.

If we look at the DSLR shipments “post Sony” from 2014, while we see a level of decline, it is certainly nothing like the decline from 2013 to 2014. This is one of the reasons looking at 2012 to current trends for DSLR’s is difficult by the pure numbers. What I find interesting is the regional breakdowns of mirrorless and DSLR’s by raw units.

We see from the DSLR shipments that the three major regions USA, Europe and Asia, all ship consistently around the same amount in volume. With Japan a consistent lower amount that hasn’t changed much over the years, especially since 2014, the post Sony era.

This fits into why CIPA reports on a USA, Europe and Asia basis, with all three areas showing consistently similar numbers and a more equal economic split between the three core areas.

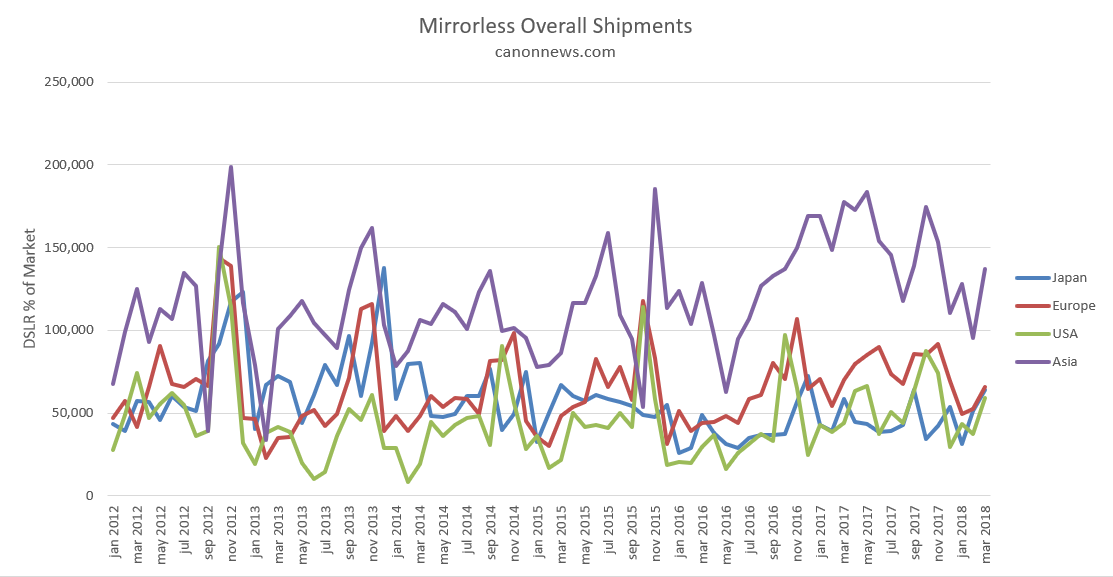

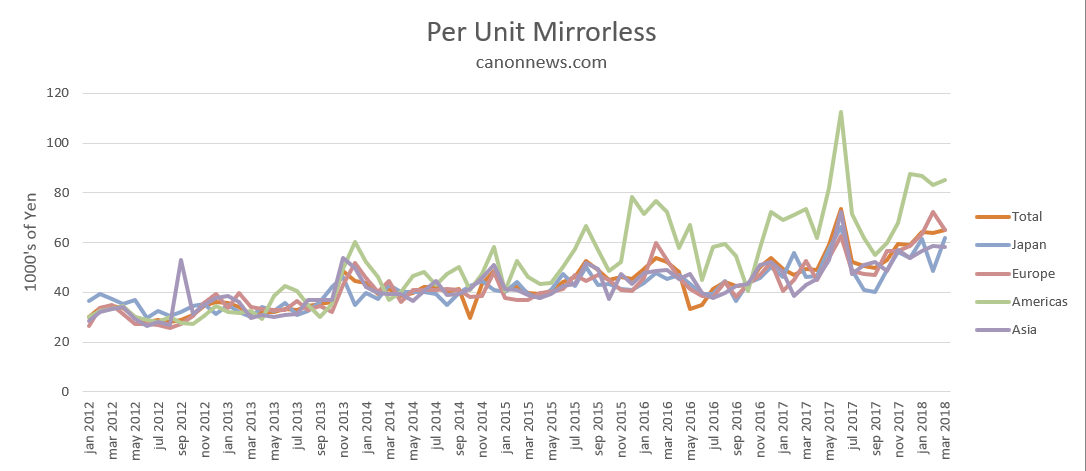

We start to look at mirrorless, and it’s a dog’s breakfast, with Asia holding significant since approximately 2015.

What’s more surprising is that the other two major economic areas, of USA and Europe are running equal to the much smaller Japan domestic market.

If you are in USA or Europe and your favorite supplier, aka Canon or Nikon is threatening to full board into mirrorless, these results should worry you a bit. You can almost guarantee that they are looking at those Asia mirrorless numbers as a prime motivation and not USA and Europe.

The USA mirrorless market still stands different than then rest of the world, as we see form unit values, the majority of higher end unit shipments still end up at the American shores while the other markets are tending to get a different product mix. Asia and Japan are slightly under the average, while Europe floats in around the average for unit value.

Whereas with DSLR’s the Asia and Japan markets are above average in product mix, and USA and Europe are below average.

Looking at this data, I feel that the mirrorless disruption isn’t as much as how mirrorless will change the industry, but more how it will change how the industry looks at markets and creates products for them.

This may be the longer learning curve for both Canon and Nikon than simply creating products.

Canon in this regard, seems to have a higher understanding, with it’s product mix maybe missing the marks for mirrorless in the more enthusiast friendly realm of Europe and USA, however, perhaps not missing the mark as much in the newer, larger economic zone of Asia.

In summary, for this month we are seeing a more consistent picture of shipments, marginal increases to mirrorless and the continued slow decline in DSLR shipments. The interesting takeaway is that when you see a camera released, and you are puzzled to why on earth the company released it, imagine how it may fit into the different markets, whether it be for DSLR’s or for Mirrorless.

Richard CanonNews

Richard has been using Canon cameras since the 1990s, with his first being the now legendary EOS-3. Since then, Richard has continued to use Canon cameras and now focuses mostly on infrared photography. Richard is the founder and editor of CanonNews since 2017, and has worked as a writer on CanonRumors and other websites in the past.

Other posts by Richard CanonNews